Tax credits in the payroll

In the payroll the aim is to pay you a certain net monthly wage that, under similar circumstances (working hours, salary), does not change during the year. That way, the employee has certaincy on net income and in general, the income tax is paid up front through payroll wage tax withholdings.

In order to accurately calculate the payroll tax withholdings, the income tax + social security contributions are calculated on the basis of the annual base wage (fixed components: salary, holiday allowance other fixed agreed allowances). Also, the annual entitlement to general tax credit and the labor tax credit are calculated on the basis of the annual base wage.

The total amount is devided by 12 months to get to the monthly payroll tax withholding and the net wage.

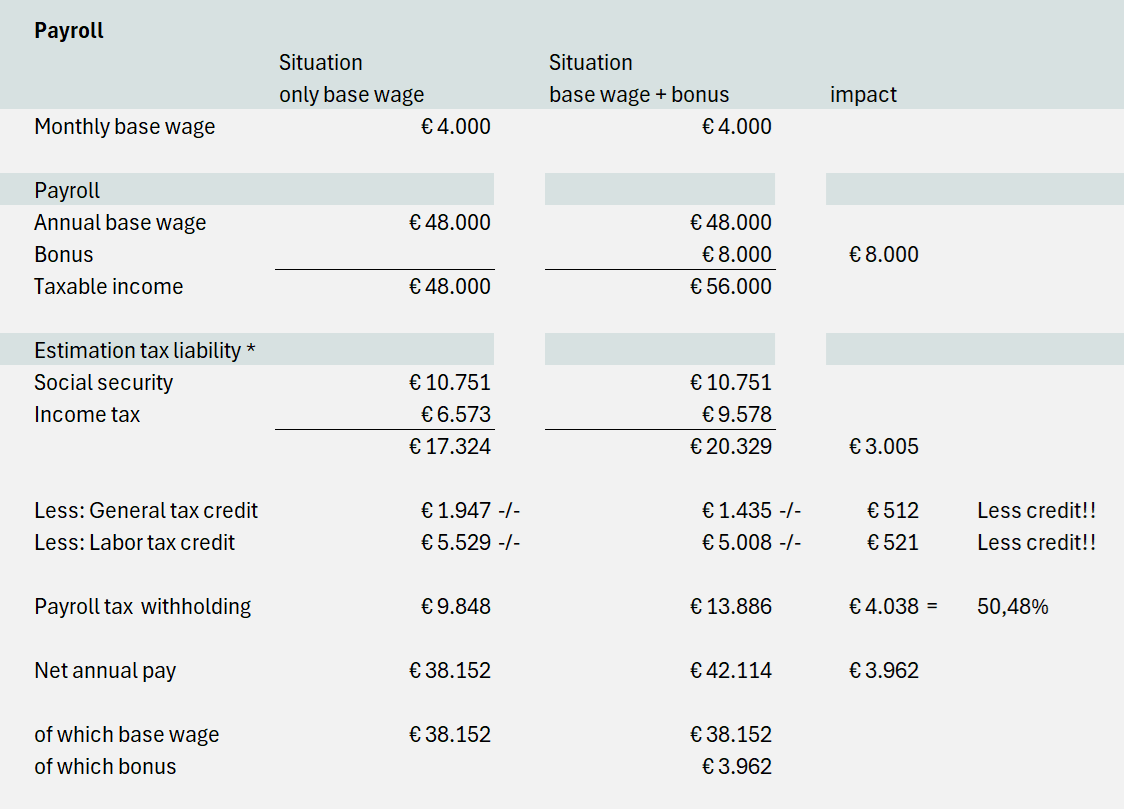

Impact of a bonus payment on tax credits (explanation of high withholding rate)

In case a bonus is paid out, the annual taxable income increases, which impacts not only the income tax + social security premiums, but also the general tax credit and the labor tax credit. These credits first grow with your income and from a certain point, the credit is reduced. A bonus payment can in this persective lead to a reduction of tax credit entitlement.

To make sure that the impact of a bonus payment does not change your net base wage, the withholding rate is adjusted. As you can see in below calculation, this can in fact lead to a withholding rate which exceeds the highest income tax rate:

Applicable income tax + social security premiums can be found here.

Tabel for calculation of the tax credits can be found here.