Personal deductions

(Persoonsgebonden aftrek)

The Dutch income tax system offers a limited range of expenses, which can be eligible for tax deduction for resident taxpayers of the Netherlands. Apart from these, there are no other personal deductions.

Charitable donations

Charitable donations to a charitable organization that is listed with the Dutch government in the ABNI register, can be tax deductible. For normal charitable donations (one time donations, monthly donation), a threshold applies of 1% of your income (in case of fiscal partners, the combined income). The excess is deducted from your taxable income (Box 1, Box 3 or Box 2).

In case of a contractual agreed periodical donation (or arranged by notarial deed) for certain fixed donation for a period of at least 5 years to a ANBI registered organization, no threshold applies.

Note that for certain "cultural organizations" with ANBI registration, 125% of the donated amount can be deducted.

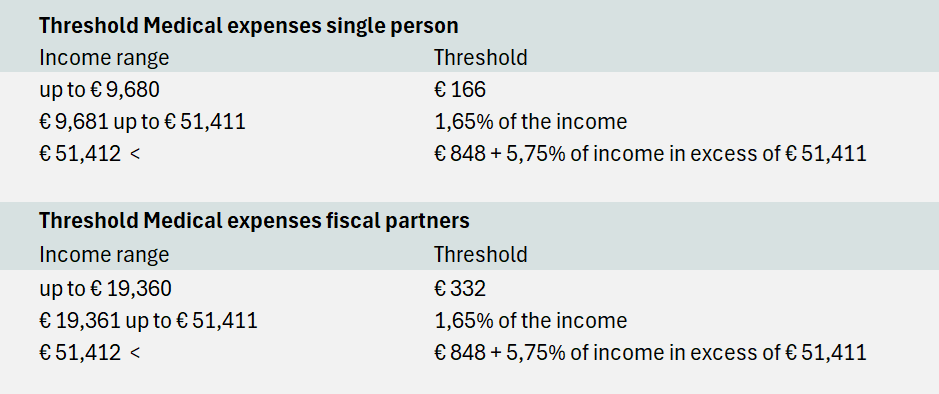

Specific medical expenses

Certain specific medical expenses, which were not covered under your medical insurance, can be tax deductable. Note that this matter is quite complex, because certain conditions apply and because not all medical expenses qualify. A specificatuion of qualifying medical expenses is listed on the website of the Dutch tax authorities.

Apart from the conditions, an income depending threshold applies, so only in case your medical expenses in the concerning year exceed this threshold, it could makes sense to look into the matter in more detail.

If your expenses were less than the income depending threshold, there is no deduction. The threshold is calculated as follows:

In case your medical expenses were more than the threshold, you can check more details (specifications and conditions) here.

Alimony to ex-partner (based on Court decision or divorce contract)

The general tax credit applies to all resident taxpayers of the Netherlands and reduces any income tax liability. This tax credit is income depending and because of the fact that the credit applies to every resident taxpayer, this credit is often considered in the payroll. The general tax credit first grows with income and from a certain amount of annual income it is being reduced. The income / credit tabel for the year 2026 for the general tax credit can be found here.

Costs of having severly disabled person(s) temporary staying in your home

In case you arrange tempoirary stay in your home for a severly disabled person who is older than 21 years of age and normally lives in a care home (Wlz instelling). Than it is possible that you can deduct certain expenses related to the stay. More details can be found here (website of the Dutch tax authorities).

Personal deductions may lower your taxable income and income tax liability. In case you were paid through Dutch payroll and wage tax was withheld, the lower liability may lead to a tax refund.

Feel free to contact us in case you have questions